While Millennials are busy complaining that they’ll never become homeowners, Gen-Z is taking the necessary steps to ensure they will be – even if that comes with risk.

Have you taken a look at the housing market recently?

From the perspective of a young professional (and depending on where you live), it might seem impossible that you could ever afford to put a deposit down on a house without splitting the cost or saving for decades to come.

Think I’m exaggerating? Promise you, I’m not. At the start of this year, the UK Office for National statistics reported the average price for a home was £274,000 – which is £24,000 more expensive than the year before.

Coupled with inflation, which is seeing the cost of living rise significantly, Gen-Z is having to redefine the age at which homeownership should happen, how they’ll get the money for it, and who they’ll be looking to share the cost with.

“ur not rich cuz you get coffee everyday” – someone who was alive when u could buy a car with a quarter u found on the floor

Looking at a survey of 875 American Millennials, many believe owning a home is more of a ‘distant dream.’ And rightly so, considering only 35.4 percent of this generation have managed to do so before the age of 35.

Despite US mortgage rates dropping to their lowest in history during the pandemic, over half of Millennials still say buying a home in the area they currently live in is ‘hard’ or ‘extremely hard’.

On top of this, a least half reported abandoning all attempts to save for down payments because they were more focused other financial obligations like healthcare insurance or student debt.

On the contrary, Gen-Z don’t share this lack of confidence towards buying homes, with 77 percent of those surveyed saying they view homeownership as being ‘at least somewhat attainable’ in the next decade.

Some researchers suggest their confidence lies in the abundance of new and different ways Gen-Z can build wealth. The rise of the gig economy, side hustle culture, cryptocurrency, and digital NFTs offer different avenues to accumulate a healthy savings without relying on physical assets.

As a result of these avenues, Gen-Z buyers experienced the biggest growth of any generation during the housing cost drop caused by the pandemic, doubling their ownership of the market from 2019 to 2020.

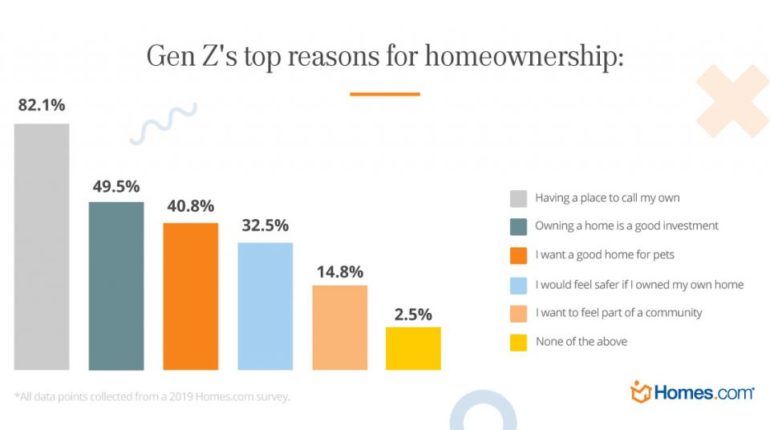

Those who aren’t quite there yet have interesting motivations. At least 82 percent call ‘having a place to call their own’ as a primary motivation for buying, with less than 50 percent wanting a home for traditional reasons: it’s a good investment.

Gen-Z are known for their will to take calculated risk. This generation is made up of well-informed buyers who have witnessed their families bounce back after multiple world-altering events such as 9/11, the financial crisis of 2008, and the pandemic.

Partnering up in a different way

Though they share different levels of optimism towards the milestone of home ownership, Gen-Z is similar to Millennials in that they still desire to own a house by the age of 30.

But unlike the generations before them, Gen-Z isn’t waiting to find ‘the one’ before they consider buying a place of their own. According to the major bank Halifax, those currently entering the housing market (ages 18 to 24) are prioritising buying a house over marriage.

We already know that Gen-Z is delaying marriage or rejecting monogamy altogether, so it should come as no surprise that some members of this generation are deciding that splitting a deposit on a house with a friend is the most secure option.

It looks like even the housing market is needing to adjust itself to the style of Gen-Z, the generation known for unapologetically breaking the status quo.

Truthfully, there’s still quite a ways to go before home-owning trends will come into full view, but it looks like friendship could be a popular option for Zoomers looking to share the financial burden of a mortgage. And which besties wouldn’t love the idea of a forever sleepover?

Deputy Editor & Content Partnership ManagerLondon, UK

I’m Jessica (She/Her). I’m the Deputy Editor & Content Partnership Manager at Thred. Originally from the island of Bermuda, I specialise in writing about ocean health and marine conservation, but you can also find me delving into pop culture, health and wellness, plus sustainability in the beauty and fashion industries. Follow me on Twitter, LinkedIn and drop me some ideas/feedback via email.

Last month, delegates, negotiators, observers, researchers, youth advocates, and representatives from civil society convened for the 64th sessions of the Subsidiary Bodies (SB64) under the United Nations Framework Convention on Climate Change (UNFCCC) in Bonn, Germany. Here are my main takeaways.

As I returned to Bonn during this year’s SB64, like most returning observers, I had expectations of technical meetings filled with dense negotiating texts and procedural debates.

Behind each...

On World Youth Skills Day, the UN has argued a changing job market calls for a new educational approach.

The world looks very different from a decade ago, when I was taking my A-Levels. Now young people are leaving school to a largely thankless job market, ill-equipped to accommodate the skills learnt through traditional education.

Technological development, the rise of AI, and a professional landscape transformed by remote working have...

The role has yet to be finalised or filled, but the government is already facing criticism over its decision to appoint a maternity commissioner.

The UK government has announced plans to appoint a maternity commissioner following ‘shocking’ failings in maternity care across England. Whoever takes on the new role will be responsible for spearheading an overhaul of the maternity healthcare system after a major review and sustained pressure from...

After pulling foreign assistance to African countries last year, Trump's government is again offering hundreds of millions in financial aid. But the support comes at a cost, and many nations aren't willing to pay it.

Ghana is the latest African country to turn down a new funding deal from the Trump administration, after the US president dismantled the governing body that oversaw foreign assistance during his second term.

Despite

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.