When did buying your first home become so unattainable and circumstantial? Young people face the devastating reality of surging property prices and laborious salary increases.

According to the World Economic Forum, countries like Switzerland and Germany consider renting the norm, where most citizens will never own the homes they live in. Historically speaking, the UK has always leaned heavily the other way.

Schroders, an investment strategy and research company, released data outlining the average property price at the beginning of 2023. The findings revealed a shockingly clear truth about average property values and their relationship with average wages.

In 2023, the former was almost nine times the amount of the latter. We haven’t seen a disparity that stark since the 1800s. A titbit verging on the impossible to stomach.

Properties fluctuate at a seemingly constant rate in the UK, and there is, unfortunately, a lot that influences the property market. Interest rates, location, government, and economic growth directly or indirectly affect the weight of a property’s price tag.

We’ve seen decades of prosperity, like the 50s and 60s when post-war Britain scrambled to build new housing to replace the rubble of the Second World War. We’ve seen soaring interest rates and prevalent unemployment in the 70s. We’ve seen markets crash, economies in turmoil, and inflation soar.

One thing we’ve never witnessed is the impossible divergence between how much we earn and how much a house costs. It’s an issue that imbues frustration and sends young people into a bottomless well of despondence.

The mid-nineties resonate with most of us in some way. All things considered, it doesn’t feel like a lifetime ago. For some of us, it marks a significant role in our date of birth; for some, it’s totemic to coming of age; for the rest, it’s a culture that heavily influenced our childhoods.

The average house in the mid-nineties reckons itself at around about £50k. The average house in 2024 is a more recognisable £300k. TheBank of England’s inflation calculator is an inflation time machine. It’s a nifty tool that allows us to see how prices in the UK have changed over time.

Properties in the mid-nineties would be worth £100k today. What’s more, if we reverse this inflation timeline, take today’s average house price, and pop it into a time machine back to when Britney and Justin were ruling pop culture, we land on £150k.

This exercise proves that inflation has grown at an unjust rate. Much like today, very few people would have been able to afford a house of that value compared to their salary.

The early noughties unwillingly laid host to a risible rise in property prices. It was around this time that privately rented homes started to make their ascension.

Rented properties have always existed in the UK; however, since 2003, renting has started to rise considerably.

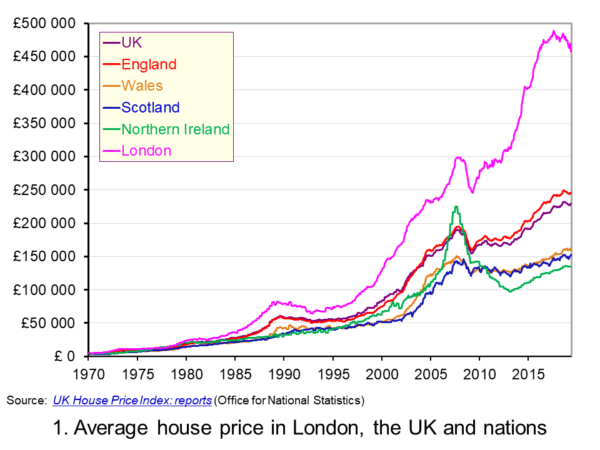

With a noticeable spike over the last few years, a pattern between the rising precarity of buying a property and the need for a roof over your head is on full display. Statista, a company dedicated to generating insights and facts across a plethora of industries, unfurls a lucid timeline of average property prices.

It’s easy to follow the rising doom of prices. I’ve focused on the English market, as this is where I am from; however, Northern Ireland, Wales, and Scotland all share a similar pattern.

If the stats shared in this article can tell us one thing, it’s that buying a house on today’s average salary is unfairly impossible. The immutable need to live under a roof, bolstered by brick and mortar, will never change. Whether your name is on the deeds of that structure is the point of contention.

Do we adopt a similar property lifestyle to the Germans and Swiss? Do only those in a couple or with hefty deposits qualify to own a house one day?

I have countless single people in my life who feel as though they’re rotting in the rental markets. Some of them are happy not to be burdened with the responsibility of a mortgage; most are fighting to escape their destitution. Having a deposit is one thing, and having the salary to back it up is another.

Many people receive a deposit under unfortunate circumstances, or perhaps, for the rare few, family can offer financial support. Even if you have the upfront cash, your property value and what you can borrow are capped by your earnings.

Let’s say you earn a London salary but can’t afford the London property alone. So, naturally, you look to commutable towns. Unfortunately for you, so is everybody else, causing the available properties in these towns to descend and their prices to ascend.

Hooray! You’ve found a property within your budget. But wait. You need to commute to your high-paying London job. Even with hybrid working permeating most industries, you’re asked to be in the office three days a week and, therefore, need an affordable rail season ticket. Affordable rail season tickets do not exist. Some of their costs are tantamount to paying rent. What about a car!? Well, what about finance, fuel, parking, and insurance?

There’s much to be said about the gaping hole in young adults’ property-owning futures. However, things are open to play with achievable mortgage products and a new leader committed to building new houses and towns – yes, whole new towns – for first-time buyers.

Our new commander-in-chief also promises to nationalise our railways within the first five years. This means cheaper fares, which makes commuter town living drastically more attainable.

If you’re a first-time buyer, explore the share-to-own options. A product that allows you to buy portions of the property over time, albeit at a cost. Converging with friends to pull together deposits and salaries is another option and perhaps a more liberally adjusted way of living.

I can’t write an article on the perils of buying a home without dropping Martin Lewis’ name into the discussion. He is a man delivered to us from the cutting-cost gods who do an unprecedented job of dishing out advice. I know I always feel a substantial amount better after listening to or reading his opinions and expert advice.

Keep our chins up and spirits high, folks. Things can indeed only get better.

Hello! My name is Fraser (he/him). I am a remote writer at Thred. Writing is an inextricable quality of my personality. When the weather is too unbearable to endure, you’ll find me writing, reading, or watching some obscure deep-dive history documentary.

As crazy as it sounds, it does add another layer to how human consumption has been impacting our planet.

For as long as humans have been on this planet, our environmental impact has become innumerable. What’s worse is that many outcomes of our actions remain unbeknownst to us, pushing us closer to the edge of an irreparable planet.

One such example is drugs, which somehow find themselves in our various waterways....

Last month, delegates, negotiators, observers, researchers, youth advocates, and representatives from civil society convened for the 64th sessions of the Subsidiary Bodies (SB64) under the United Nations Framework Convention on Climate Change (UNFCCC) in Bonn, Germany. Here are my main takeaways.

As I returned to Bonn during this year’s SB64, like most returning observers, I had expectations of technical meetings filled with dense negotiating texts and procedural debates.

Behind each...

On World Youth Skills Day, the UN has argued a changing job market calls for a new educational approach.

The world looks very different from a decade ago, when I was taking my A-Levels. Now young people are leaving school to a largely thankless job market, ill-equipped to accommodate the skills learnt through traditional education.

Technological development, the rise of AI, and a professional landscape transformed by remote working have...

The role has yet to be finalised or filled, but the government is already facing criticism over its decision to appoint a maternity commissioner.

The UK government has announced plans to appoint a maternity commissioner following ‘shocking’ failings in maternity care across England. Whoever takes on the new role will be responsible for spearheading an overhaul of the maternity healthcare system after a major review and sustained pressure from...

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.