As we make the transition to a greener world and the costs of climate change continue to rise, the public and private sectors have agreed to start paying their fair share. But will these promises be met with real action?

When attempting to solve climate change, it’s important that we not lose sight of the fact that millions around the world are already feeling its effects.

Without sufficient financial means to develop sustainably and adapt to widespread droughts, flooding, and more, the well-being and livelihoods of those living in low and middle-income countries continue to be threatened.

So as much as we want to avoid playing the blame game, at the end of the day, it isn’t these countries who have and continue to contribute most to climate change. They are, in fact, paying the highest price.

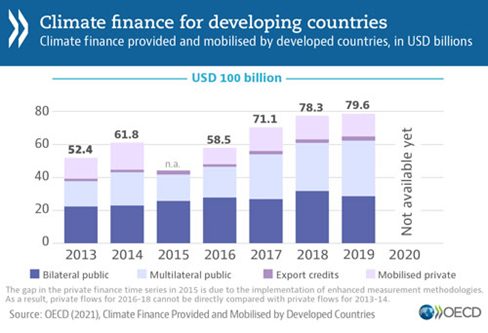

In light of this, 12 years ago, high-income countries pledged to mobilise $100 billion USD a year in climate finance by 2020. But in 2019, they only managed to follow through with $79.6 billion USD.

Credit: OECD

Having fallen short on their promise, these countries are now in a position to reassess their commitments at COP26 and show the world that they are serious about righting one of the greatest inequalities of climate change.

In the lead up to COP26, the UK called for high-income countries to deliver on their promise. But this money isn’t only meant for adapting to climate change. Commitments to public finance moving forward must also include building new markets for mitigation and adaptation, and improving access to finance for communities around the world looking to take climate action.

And what does this mean for receiving countries? It means cheap, reliable, and renewable clean electricity for schools in rural Africa, better infrastructure and defences against storm surges for the Pacific islands, improved access to clean water in Southeast Asia, and more.

Is public investment enough?

Not according to Rishi Sunak, finance chancellor of the UK, who acknowledged the need for both public and private finance to ensure that the 1.5 C goal be met. With a need to deploy the investments necessary to combat climate change, countries around the world plan to accelerate three actions.

The first is to be an increase in public investment and more collaboration between developed and developing countries, as well as a renewed pledge of $100 billion USD a year by 2025.

The second, mobilising private finance, has already begun to show some progress. Sunak recently announced that the Glasgow Financial Alliance for Net-Zero (GFANZ) now consists of over 450 firms representing $130 trillion USD. That’s nearly double the $70 trillion USD when GFANZ was launched in April.

These firms must now commit to using science-backed guidelines to reach net-zero carbon emissions by 2050 and provide 2030 interim goals.

The final action will be rewiring the global financial system for net-zero. This includes things like proper climate risk surveillance, better and more consistent climate data, etc.

But this is all easier said than done. According to United Nations Secretary-General Antonio Guterres, ‘there is a deficit of credibility and a surplus of confusion over emissions reductions and net zero targets, with different meanings and different metrics.’

There are also concerns over greenwashing and monitoring which, if not addressed effectively, may lead to more unfulfilled promises.

Many, however, remain hopeful that both private firms and high-income countries will do their part in financing a just and equitable transition to a green world. So as we continue to hear promises, promises, and more promises from leaders at COP26, it is critical that we also continue to demand real action.

This article was guest written by Ghislaine Fandel, the Science Communication Lead & Content Director at ClimateScience. View her LinkedIn here.

I’m a contributing writer here at Thred. My bio and contact information can be found at the bottom of each article. If you would like to become a remote writer for Thred, please email us at [email protected] or click here to see more information on the Change Maker Network.

The ongoing Winter Olympic Games have seen many acts of defiance against the Trump administration. How will the situation play out when the US hosts in 2028?

When Baron Pierre de Coubertin revived the Olympics in 1896, one of his main aims was to promote mutual understanding among athletes. He believed that competing on the track instead of the battlefield could encourage peace and help prevent war.

However, countless...

Anxiety, depression, and emotional problems are on the rise across the globe, cutting across boundaries of culture, geography, and socio-economic status. The World Health Organisation says ‘one in seven’ have a mental health disorder in 2026.

According to the World Health Organisation, ‘one in seven adolescents worldwide has a mental health disorder.’ Such statistics obviously cannot be ignored.

This generation of teens is the first to be raised in an...

Why has the precedent that ‘British culture is dying’ invaded every aspect of our lives recently? From TikTok commentary to culture-war politics, who is really influencing the supposed shift in British culture?

Claims that Muslims and BAME communities are erasing British culture have become a popular rhetoric in recent political spheres in the UK, but also around the Global North as a whole. Popular, but not new.

Here's my take...

Findings suggest women' s professional development was only a priority for half of US businesses in 2025.

‘Many companies are overlooking women – and it’s crucial that they don’t,’ reads the opening line of the 2025 Women in the Workplace report. What follows is no more encouraging. The state of play across the corporate landscape is pretty dire where gender parity is concerned.

The standout finding was that only half...

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.